US factories begin to fire up again

Updated: 2011-11-11 09:05

By Harold L. Sirkin, Michael Zinser, Douglas Hohner and Justin Rose (China Daily)

|

|||||||||

American manufacturing is on the way back, and that is not necessarily a bad thing for China

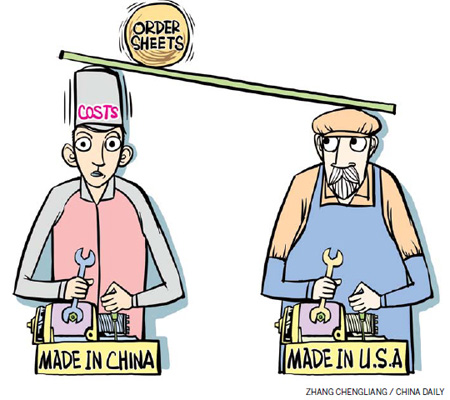

China's manufacturing cost advantage over the United States is shrinking.

Within five years, our research indicates rising Chinese wages, higher US productivity, a weaker dollar and stronger renminbi, and other factors will close most of the cost gap between the US and China for many goods consumed in North America.

As a result of these changes, we expect that many US companies will rethink their sourcing strategy. Some will likely bring China production back to the US. Others will reconsider plans to move production abroad. Companies will make decisions based on total costs, rather than just factory wages. For many products sold in North America, the new maths will give the advantage to the US, triggering a resurgence in US manufacturing.

Given the strength of the Chinese economy, however, domestic plant closures are unlikely; production will simply be repurposed for domestic and regional consumption.

Transportation goods, such as vehicles and automobile parts, electrical equipment including household appliances, and furniture are among the sectors most likely to rebound in the US. Others include plastics and rubber products, machinery, fabricated metal products and computers and electronics.

These seven sectors alone account for about $2 trillion in US consumption and some 70 percent of US imports from China.

Altogether, we estimate the US manufacturing rebound could add some 2 to 3 million jobs to the US economy, reducing unemployment by 1.5 percent to 2 percent relative to today's levels. US economic output would also be boosted, by an estimated $100 billion per year, and the impact on the US non-oil merchandise trade deficit would be to lower it by 25 percent to 35 percent.

What is driving the shift?

The first item is labor costs. Wage and benefit increases of 15 percent to 20 percent per year at the average Chinese factory will reduce China's labor-cost advantage over low-cost US states from 55 percent today to less than 40 percent in 2015, when adjusted for the higher productivity of US factory workers.

Because labor accounts for a small portion of a product's total costs, the savings gained from outsourcing to China will likely drop to single digits for many manufactured goods.

A second major factor is transportation and the costs of a longer supply chain. When transportation, duties, supply chain risks, industrial real estate, and other costs are fully accounted for, the cost savings of manufacturing in China dwindles even further. This is becoming the new reality.

Automation and other measures to improve China's productivity, which has been growing at nearly five times the pace of US productivity, won't be enough to preserve China's cost advantage. Indeed, automation and other productivity-enhancing measures will undercut the primary attraction of outsourcing - access to low-cost labor.

This good news for America should not be seen as bad news for China. In the grand scheme of things, China's position as the premier hub for low-cost manufacturing will not change substantially. For many products, manufacturing in China will remain the most attractive choice because of China's technological leadership, economies of scale and industrial clusters.

More Chinese production will be devoted to supplying China's burgeoning domestic market, which is gaining millions of new middle-class households each year, as well as other fast-growing economies in Asia. China will also likely continue to remain a low-cost supplier to Western Europe.

But China's reign as the automatic "default" choice for low-cost manufacturing is coming to an end.

For instance, when it comes to products that are mass-produced and labor-intensive, like apparel and shoes, China will be challenged by lower-cost manufacturers in emerging Africa, Indonesia, Vietnam and Mexico. But there are limits to how far it will go. The ability of these nations to absorb the higher-end manufacturing that now goes to China will be limited by inadequate infrastructure and domestic supply networks, scarcity of skilled workers, and lack of scale.

The US is a different matter. When all costs are taken into account, including production, quality control, and transportation, America's lowest-cost states will emerge (and are already emerging) as China's strongest challengers. These states are now some of the least expensive production sites in the industrialized world, which will lead more and more companies to consider the US when they are looking to increase production capacity.

Such a shift can already be seen. NCR, for example, has moved production of its ATMs from China to a plant in Georgia. The Coleman Company is moving production of certain plastic coolers from China to Kansas. Ford Motor Company is adding 12,000 jobs at its US manufacturing facilities, including some from work that would have been done in China and elsewhere, as part of an agreement with the United Auto Workers union. Sleek Audio has moved production of its high-end headphones from Chinese suppliers to a plant in Florida.

As the only major industrialized nation not leveled by World War II, the US accounted for approximately 40 percent of the world's manufactured goods in the early 1950s. Then the bottom seemed to fall out. Fueled by relentless waves of imports from Europe and Japan, the US experienced a dramatic loss of market share in industries such as color TVs, steel, cars, and computer chips.

By the 1970s and 1980s, fears of the loss of US industrial competitiveness were particularly acute, prompting a widespread debate over whether the US should adopt a "Japan Inc."-style industrial policy and teach its schoolchildren to speak Japanese. Then came the rise of such "East Asian tigers" as South Korea and Taiwan region. This led to the massive transfer of production, from the US to East Asia, of many labor-intensive goods, including clothing, shoes, and toys. Much of the US computer and consumer-electronics industries followed.

Unlike most nations, however, the US allowed industry to adapt. Factories closed, companies failed, banks wrote off losses, and workers had to learn new skills.

US industry responded with surprising flexibility and speed to reemerge more competitive and productive than ever. By the late 1990s, US companies dominated the world in high-value industries such as microprocessors, aerospace, networking equipment, software, and pharmaceuticals.

Today, US manufacturing is in the midst of a similar process of readjustment in response to China's emergence as a major player on the global manufacturing stage.

These developments occurred in a remarkable breadth of industries, from labor-intensive assembly work to heavy industry and high-tech.

These trends do not suggest that Chinese manufacturing will decline or that multinational companies will shut their mainland plants. A US resurgence will not diminish China's role as a global manufacturing power.

Harold L. Sirkin is a senior partner of The Boston Consulting Group (www.bcg.com), a global management consulting firm. Michael Zinser and Douglas Hohner are BCG partners, and Justin Rose is a BCG principal. The opinions expressed in the article do not necessarily reflect those of China Daily.