Borrowers face costly payback

Updated: 2012-02-14 07:56

By Li Jing and He Na, and Xu Junqian (China Daily)

|

||||||||

|

|

|

|

Death sentence for ex-tycoon fuels debate over private lending, report Li Jing and He Na in Beijing, and Xu Junqian in Zhejiang.

Wu Ying used to be one of the richest women in China. Today the former billionaire is on death row.

In the eyes of many people, particularly the judge who threw out her appeal last month, Wu is a fraudster who swindled her friends and business partners out of 770 million yuan ($122 million).

Yet, others oppose the sentence and say her case highlights a major issue in China: the reliance among small- and medium-sized enterprises on high-interest loans from private lenders.

From loan sharks and underground banks to pawnshops and auction houses, the private lending chain is huge and diverse, according to economists, who blame the situation largely on the struggles experienced by entrepreneurs in getting startup funds through authorized channels.

After 30 years of ongoing reforms, experts are now adding their voices to calls for China's financial sector to be opened up even further.

On Jan 18, Zhejiang province's high court upheld the death penalty handed down to Wu, insisting that the 31-year-old had purposefully cheated lenders between 2005 and 2007, using false financial statements and promises of large returns.

"Her intention was to defraud, this was more than just illegal fundraising," said presiding judge Shen Xiaoming on Feb 7, in a statement issued in response to public opposition to the sentence.

Yet, Hu Xingdou argues differently. The professor of economics at the Beijing Institute of Technology said that as tightened monetary policies have made it tough to get bank loans, borrowing money from relatives, friends and acquaintances on the promise of high returns has become the only option for many Chinese entrepreneurs.

Most long-term lending by commercial banks only goes to government-backed projects, which carry less risk, he said. All that is available to small and medium-sized enterprises, such as those run by convicted tycoon Wu Ying, is short-term capital that cannot be invested in fixed assets.

Although it is illegal and unregulated, he said private financing might actually be complimenting the official system.

"Interest rates are sometimes much higher than those set by State-owned banks, but the 'application' process is flexible and straightforward," Hu added.

Tightened policies

Xinhua News Agency recently reported on a survey of 2,835 SMEs in Zhejiang province done late last year that found almost all of them had had difficulty getting loans. (The report did not reveal who conducted the study.)

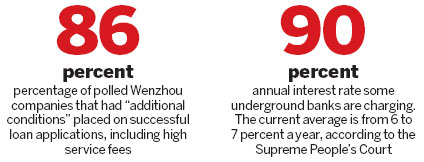

About 15 percent had seen applications to commercial banks either rejected or "downsized", it said. And for those who did get loans, 86 percent said there were "additional conditions", such as a requirement to buy financial products or pay high consulting and service fees, which pushed up the cost.

Ultimately, the findings in the Xinhua report showed companies are being pushed into the arms of private lenders, who offer fewer rules but higher interest.

The Supreme People's Court deems private lending illegal when the interest rate is four times higher than that of a commercial bank. Yet, while the current average is from 6 to 7 percent a year, some underground banks are lending at an annual rate of up to 90 percent.

According to the survey of Zhejiang businesses, roughly 9 percent of respondents said they "frequently" borrow from private lenders to ensure cash flow, with 47 percent doing it "occasionally".

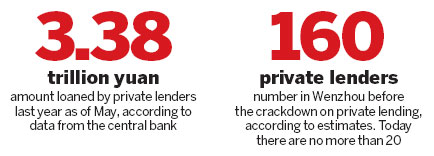

The most recent data from China's central bank also supports this theory. It stated that private lenders had loaned 3.38 trillion yuan ($536 billion) last year by May.

One of Zhejiang's most vibrant industrial hubs is Wenzhou, where economists say underground banks have become a lifeline for small businesses.

Despite a robust economy and a large collection of nouveau riche, the city's largely light industry relies heavily on labor, and therefore is often passed over for loans by official financial institutions.

"In Wenzhou, 90 percent of enterprises need private lending to get their production lines running. It's high time to legalize private lending," said Zhou Dewen, director of the Wenzhou Small and Medium-sized Enterprises Development Association. "It's not that businesspeople prefer private lending to (commercial) bank loans, but they have little option."

Open to abuse

Without a proper monitoring system, however, experts warn that private lending poses a threat to the health of China's economy.

Private lenders enjoy no legal protection, meaning that unpaid loans often result in disputes and, in extreme cases, violence. Meanwhile, the existing system is also open to money launderers.

Authorities have been cracking down on the illegal practice since October, when a number of Wenzhou bosses fled or killed themselves to avoid paying back high-interest loans. Now that the tap has been turned off, small business in the city has been hit even harder. The owner of a shoe factory, which has been in operation since 2003, told China Daily that this year is the first time he has been unable to restart the production lines immediately after the Spring Festival holiday.

"We just don't have enough money," he said, on condition of anonymity. "Without cash flow, we cannot and dare not hire people and receive orders."

With the rising costs of labor and materials and the tightened bank policies, he said that the government crackdown on private lending had been the last straw. "We just hope something concrete can be done sooner or later," he added.

According to Zhou's association, Wenzhou until recently had about 160 private lenders and "guarantee organizations", which are companies or individuals who stand as guarantor on loan applications. Today there are no more than 20.

One lender, who gave his name only as Fu, said he will not even lend money to relatives nowadays, explaining that once the money is "out of my hand, I have little chance of ever seeing it again".

Nine out of ten lenders mostly bankrupt bosses will take the money and flee, he said, adding: "It's a vicious circle."

Legalization of private lending is urgently needed, said Zhou, as well as moves to create more financing options for small and medium-sized enterprises, such as relaxing monetary policies on private banks.

He Tian, a real estate developer based in Zhejiang, agreed. "In some ways, we're luckier than the manufacturing industry, as we barely rely on private lending. Yet, we still need it for emergencies," he said. "The sooner it is regulated, the better and safer it is for both creditors and debtors."

Economists, legal experts and sociologists from across China met to discuss the implications of Wu Ying's case at two seminars in February. Most echoed the call for legalization.

"Private financing has supported the development of China's private sector, so it is worth recognition by the authorities," said Hu at the Beijing Institute of Technology. "That's why Wu's case has attracted so much public attention."

Final decision

The fate of former tycoon Wu now lies with the Supreme People's Court, which is reviewing her case. Hu argues that if her execution is approved, the monopoly by State-owned banks can be further consolidated and would deal a heavy blow to the country's burgeoning private sector.

"Instead, the government should admit the legal status of private lending, support those with good records and establish a set of criteria to bring underground banks to the surface," he said. "This way, it will be easier to monitor and regulate."

There is also no clear legal boundaries between illegal fundraising and reasonable private lending, a fact that has fueled opposition to Wu's death sentence, he said.

Wu grew up in Dongyang, a city in Zhejiang, and started her working life in a relative's a hair salon in 1997.

Within a decade, she was running a conglomerate of hotels, car dealerships and real estate, and was regarded as the country's sixth-richest woman.

At the time, she represented a success story of the robust entrepreneurial spirit that could typically be found in the coastal province in East China.

"Many questions are still left unanswered in Wu's case," Hu said. "For example, she only collected money from 11 lenders, two of whom were her business group's senior executives. They were fully aware of the financial situation.

"How can it be defined as fraud?"

The reporters can be contacted at lij@chinadaily.com.cn, hena@chinadaily.com.cn orxujunqian@chinadaily.com.cn

Relief reaches isolated village

Relief reaches isolated village Rainfall poses new threats to quake-hit region

Rainfall poses new threats to quake-hit region Funerals begin for Boston bombing victims

Funerals begin for Boston bombing victims Quake takeaway from China's Air Force

Quake takeaway from China's Air Force Obama celebrates young inventors at science fair

Obama celebrates young inventors at science fair Earth Day marked around the world

Earth Day marked around the world Volunteer team helping students find sense of normalcy

Volunteer team helping students find sense of normalcy Ethnic groups quick to join rescue efforts

Ethnic groups quick to join rescue efforts

Most Viewed

Editor's Picks

|

|

|

|

|

|

Today's Top News

Health new priority for quake zone

Xi meets US top military officer

Japan's boats driven out of Diaoyu

China mulls online shopping legislation

Bird flu death toll rises to 22

Putin appoints new ambassador to China

Japanese ships blocked from Diaoyu Islands

Inspired by Guan, more Chinese pick up golf

US Weekly

|

|