View

Normalize monetary policy

By Louis Kuijs (China Daily)

Updated: 2010-12-10 08:00

|

Large Medium Small |

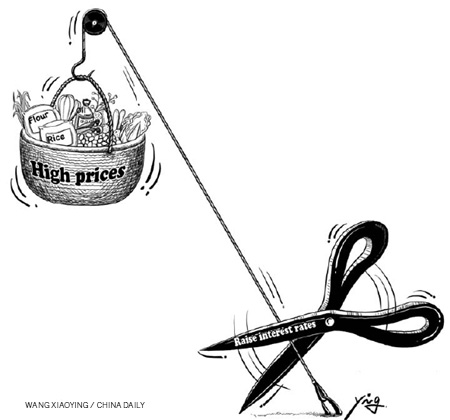

The recent rise in China's inflation has grabbed the attention of the public and policymakers alike. Consumer price inflation rose to 4.4 percent in October and a further increase is expected. This is higher than we are used to in China, although it is modest in an emerging market perspective. To determine the best policy response to the rise in inflation it is important to know its cause and how much inflation we should expect in the coming 12 months. It is also good to decide what an acceptable rate of inflation is for a country like China.

So far, the rise in inflation is because of higher food prices. The food component of the consumer pice index in October was up 10.1 percent year-on-year, contributing two-thirds of overall inflation, while non-food prices were up 1.6 percent on this basis. In looking for the cause of the higher food prices, monetarist explanations are common.

After the massive monetary expansion since the end of 2008 there is a lot of liquidity sloshing around, potentially putting upward pressure on prices, especially asset prices. In this setting, there are reports that speculative activity has driven up prices of several food products.

It is also true that in the long run sustained monetary expansion drives up inflation. However, the link from money to inflation is more indirect and complex than simplistic monetarist interpretations suggest and, in the meantime, inflation is basically determined on the markets for goods and services.

Several food markets have been buffeted by domestic supply shocks. In particular, vegetable prices, which have seen the largest price rises, have been hit by bad weather and natural disasters. Recent hikes in international food prices have added pressure. China's rice and wheat prices do not closely follow international prices, since they are managed by policymakers.

However, prices of corn and soybeans in China follow international prices fairly closely, and higher prices for these products have helped raise meat and egg prices. Housing-related costs have also contributed. However, prices other than those of food and housing remain contained - in October, they were up 0.8 percent year-on-year.

Inflation is unlikely to escalate but expectations matter and there are risks. Food prices are unlikely to continue to rise at the recent pace. Domestically, the supply side factors driving up prices are considered in large part temporary. Internationally, after the hefty increases in prices of raw commodities such as food and many industrial commodities since early summer, mainstream forecasters do not expect them to continue to increase at this pace.

More generally, despite further quantitative easing in the US, global inflation prospects are generally considered modest, largely because of substantial spare capacity in many markets globally. Indeed, the US just registered the lowest rate of core inflation since records began in 1957.

There is some risk that the higher food prices will spill over into wages and other prices. This risk is manageable but it requires policy attention. People typically resist real wage declines if they can. Thus, large rises in prices of food or energy are often followed by wage hikes. This can set in motion a wage-price spiral, especially in a low productivity growth environment.

In China, price shocks tend to be more easily absorbed than in many other countries because of robust productivity and wage growth, and core inflation is low to start with because of the rapid productivity growth in industry. Nonetheless, with inflation expectations having risen substantially and the labor market less loose than it used to be, macroeconomic policy will need to play an important role in limiting the spillover of food prices into other prices and wages.

The risks of inflation and the need to manage inflation expectations strengthen the case for normalizing the monetary stance. Indeed, with little spare capacity in China's economy, respectable growth prospects, and concerns about too rapid housing price increases, this normalization will need to be a central objective of macroeconomic policy.

Thus, after the spectacular increase in monetary aggregates since the end of 2008, monetary growth will before long need to come down to rates broadly similar to nominal growth.

Moreover, relying more on interest rates and less on quantitative instruments such as credit controls would help reduce the underlying pressures on asset prices and reduce distortions. In October, People's Bank of China raised benchmark interest rates by 25 basis points. But they are still much lower than before the crisis and they will have to go up more.

Concerns about the impact of financial capital inflows are overdone and are no good reason not to increase interest rates. Thanks to China's largely effective capital controls, the amount of net financial inflows (called "hot money" in China) is actually very low compared to domestic credit creation. Also, the overwhelming majority of the increase in foreign reserves is not from net financial capital flows but from current account surpluses and net foreign direct investment.

However, the inflation outlook does not seem problematic enough to warrant surpressing overall inflation by administrative measures or postponing needed price adjustments. High inflation is distortive and not helpful. However, in rapidly growing countries like China, relative prices need to change to facilitate changes in the economic structure. In most emerging markets moderate inflation - of 4-5 percent - is not seen as a major problem.

Constraining inflation to be very low could hinder helpful relative price changes. For instance, China needs to increase administrative prices for resources and utilities - especially energy and water - to help adjust the structure of the economy. And, higher prices for agricultural products and higher migrant wages can help boost rural incomes and reduce urban-rural inequality, thus helping to improve the primary income distribution.

It would be really unfortunate if such desirable developments were suppressed because of concerns about moderate inflation. Thus, somewhat higher tolerance to modest inflation could help bring about some of the structural reform and change that the government is aiming for.

The author is a senior economist at World Bank Office in Beijing.