View

Realty market faces dilemma

By Fulong Wu (China Daily)

Updated: 2010-12-15 08:04

|

Large Medium Small |

A heated debate is raging on what should be the best policy for the housing sector in 2011 given the skyrocketing housing prices. The best strategy would be to avoid a hectic property boom, because the hope of reducing prices to solve the affordability problem is only an illusion.

According to the "Blue Paper" of the Chinese Academy of Social Sciences on the Chinese economy, housing prices will see a "retaliatory price rebound" in 2011 if the government were to relax measures aimed at cooling the market. Prices could rebound by 20 to 25 percent next year. The increase, however, has been forecast in the context of widespread 29.5 percent overpricing in 35 large and medium-sized cities, the "Blue Paper" said.

Clearly, the property boom will not be driven by robust and rational demand. Last year, we could blame the inflow of capital into the property market because of the sluggish export-based manufacturing industries and hence the shifting of capital investment from the real economy to "fictitious accumulation" and "international hot money". Subsequently, the government adopted more stringent measures to constrain capital shift, thus cooling down the housing market this year.

But November was the third consecutive month when prices increased. Property prices in 70 major Chinese cities increased 0.3 percent month-on-month, according to data just released by the National Bureau of Statistics. This seems to confirm the trajectory that the Chinese Academy of Social Sciences predicted.

So what will be the prospects of the housing market next year? No doubt, we will continue to see forceful pressures for a boom. But such pressures come from not only investors' motivation for making profit, but also consumers' fear of inflation. On Dec 11, the National Bureau of Statistics released the consumer price index for November, which increased to a 28-month high of 5.1 percent. The figure provides a clue: the expectation for a boom in the housing market could mean a self-fulfilling myth.

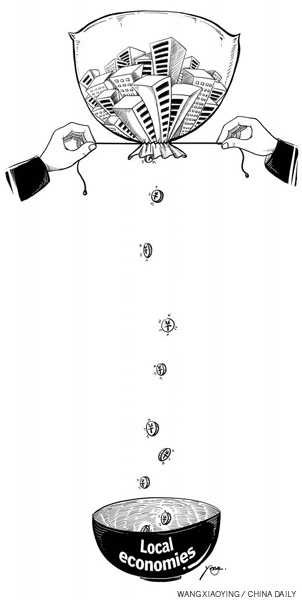

Should the government take more strict measures? The tricky issue is that the housing market is tightly embedded in the local growth-oriented regime. Now it is more an art than rocket science to gauge a proper level of control. The target set by the government to regulate the housing market in such a way that prices rise slowly and modestly would now be hard to achieve, because it strives to provide some certainty of value appreciation in a very uncertain environment - an environment in which we do not know how to avoid value depreciation during inflation. This may in turn unexpectedly blow up the property bubble.

It would be a clich to suggest that housing prices could not be predicted. This is particularly true in the current situation, because the price changes are affected by many policy uncertainties. It is more complicated than gauging demand and supply. For example, migrant workers' demand for housing depends upon the hukou (house registration) reform and the progress of migrants' integration into cities.

More than that, housing consumption is closely related to (perceived) inflation. Nowadays, more affluent households adopt a coping strategy of using property to invest for the future. For them, buying a house is not different from buying a piece of antique.

Nevertheless, the current rental yields are too low to justify housing as an outlet for capital investment. The purchase of housing depends entirely on value appreciation or capital gain. The prospect of rising inflation would strengthen the view that housing investment is a long-term safe haven for capital gain.

The policy regulation, therefore, is to clear any bottleneck in the supply line that may artificially boost such investment for capital gain even in the short term. A policy that reduces the fluidity of the housing market would be useful, too.

The policies could include building more affordable houses, reforming the land-centered local fiscal regime and creating a multi-layered housing system, which would be sufficient to maintain overall stability of the housing market, while permitting usual price fluctuations and making the risk of using housing as asset investment more transparent.

An overheated housing market would increase the financial risk, thus creating fluctuations in the overall economy. While it is common perception that an affordability issue may even engender social stability - it is more a discourse of middle-class high-priced entrance into the commodity market rather than a fact that may imply a solution to the housing price adjustment problem. But expecting price adjustments may be only an illusion.

The best scenario for the housing market next year would be neither boom nor burst. There should be no guarantee for investors' asset valorization, either. At the end of day, it is such a myth in the era of inflation that could be self-fulfilling.

The author is a professor and director of Urban China Research Centre at Cardiff University, United Kingdom.