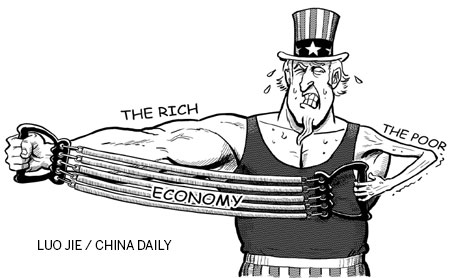

Income gap the bane of US

Updated: 2013-08-13 07:27

By Kemal Dervis and Uri Dadush (China Daily)

|

||||||||

US President Barack Obama has just committed himself and his administration to fighting the scourge of income inequality. Indeed, it is not a moment too soon to focus on this issue.

The United States' recovery has been incredibly unequal, with the incomes of the richest 1 percent growing robustly, while those of the bottom 99 percent are stagnant. For a long time, few economists - even those who worried about inequality - have deliberated this topic in the context of macroeconomic policy.

As it turns out, high and rising levels of inequality may well be a cause of increased macroeconomic instability. But the negative spiral doesn't end there; high inequality also contributes to a fraying of the political consensus, is associated with boom-bust credit cycles and may ultimately lead to a chronic weakness of economic demand.

The US is now caught in a vicious cycle. The cycle starts with stagnant incomes and a biting credit constraint (there is no other word to put it appropriately) at the middle and low end of the income distribution. As dramatically exemplified by the large numbers of continuing and still unresolved home foreclosures, this has led to low expectations for effective demand growth - and therefore low business investment in the US economy at large.

The US Federal Reserve has been trying to stimulate demand via monetary policy with very low interest rates or "quantitative easing", or with both. However, these measures have been of dubious efficacy. According to the old adage, you can lead a horse to water, but you can't make it drink.

In addition, there is a pronounced risk of re-igniting an unsustainable borrowing process. The bottom 90 percent of American households, with incomes still stagnant, is not yet in a considerably better position to borrow. Yet this is what is heralded - whether to pump up car sales or whatever else.

Moreover, very low interest rates may worsen the distribution of income in the US. How so? They lead to low or negative real returns on small savings of a large number of people, while they reduce the cost of borrowing by companies owned disproportionately by relatively wealthy individuals.

So companies can borrow at zero real rates and invest at much higher returns. Also, stock prices have been rising dynamically, benefiting all those with a stock market portfolio. However, most people in the "lower 90 percent" of US households don't have any sizable portfolios.

Besides, the option to pursue an expansionary fiscal policy (for example, by spending more on infrastructure) as well as increased spending on unemployment benefits (and other elements of the social safety net) are constrained by concerns over rising public debt.

The US may thus have reached a point where the classic arsenal of counter-cyclical policies has become much less effective. To an appreciable degree, this grave problem is due to what has become a structural form of income concentration that initially helped trigger the global financial crisis and now limits a sustainable growth path in broad-based private demand.

If this interpretation is correct, then it is the rebalancing of the distribution of income within the US that would play a key role in unlocking the US economy's growth potential in a sustainable way. This kind of "internal rebalancing" stands in stark contrast to "global rebalancing", which is so often touted by the US Treasury and many mainstream economists as the solution to the country's current woes.

Because the US is a large economy relatively less exposed to the global economic cycle (exports only account for about 12 percent of GDP), the idea that, for example, expansion of demand in China could play a big role in re-igniting US growth was always far-fetched.

Estimates of fiscal stimulus multipliers in the US and elsewhere provide strong evidence in support of the view that increasing the purchasing power of those at the lower end of the income spectrum could make a real difference. Social balancing programs, such as the Earned Income Tax Credit, food stamps, unemployment benefits and work-share, provide transfers to boost the incomes of low-income or unemployed groups.

These instruments are believed to be four to five times as effective in stimulating demand as policies that benefit high-income groups, such as tax cuts for those with high incomes, for corporations and in the capital gains arena.

This is not a new insight. It was Henry Ford who recognized that it made sense to pay his workers enough so they, too, could buy the cars they produced.

An economy such as the US', where nearly all of the income growth accrues to the very rich, is unlikely to generate a corresponding growth in broad-based demand, especially after the global financial crisis ravaged the credit scores of a large percentage of the middle class and the poor in the country.

Kemal Dervis is director of the Global Economy and Development Program at the Brookings Institution and Uri Dadush leads the International Economics Program at the Carnegie Endowment.

They are contributors to The Globalist The Globalist.

(China Daily USA 08/13/2013 page12)

Most Viewed

Editor's Picks

|

|

|

|

|

|

Today's Top News

Academy will turn a Hilton into a dorm for Chinese

Research funds spread across the globe

Reps gear up for TPP round 19

Brazil puts off bidding on bullet train

US to examine intelligence collection methods

Rare earth alliance to fight Japan's patent barrier

Economists cautious about China's recovery

Terrorist leaders sentenced to death

US Weekly

|

|