No doubling down on old model

Updated: 2013-05-03 07:10

By Stephen S. Roach (China Daily)

|

||||||||

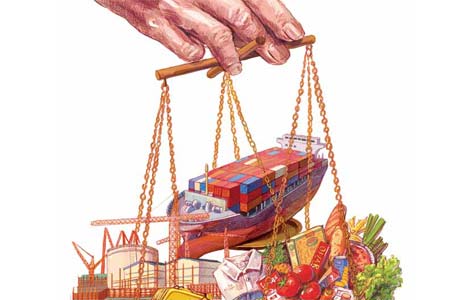

Other countries will need to adapt as China embraces slower economic growth as a result of its rebalancing

At 7.7 percent, China's annual GDP growth in the first quarter of this year was slower than many expected. While the data were hardly devastating relative to a consensus forecast of 8.2 percent, many expected a second consecutive quarterly rebound from the slowdown that appeared to have ended in the third quarter of 2012. China doubters around the world were quick to pounce on the number, expressing fears of a stall, or even a dreaded double dip.

But slower GDP growth is actually good for China, provided that it reflects the long-awaited structural transformation of the world's most dynamic economy. The broad outlines of this transformation are well known - a shift from export- and investment-led growth to an economic structure that draws greater support from domestic private consumption. What is less well known is a rebalanced China should have a slower growth rate, the first hints of which may now be evident.

A rebalanced China can grow more slowly because by drawing increased support from services-led consumer demand, China's new model will embrace a more labor-intensive growth recipe. The numbers seem to bear that out. China's services sector requires about 35 percent more jobs per unit of GDP than do manufacturing and construction the primary drivers of the old model.

That number has potentially huge implications, because it means that China could grow at an annual rate of 7 to 8 percent and still achieve its objectives with respect to employment and poverty reduction. China has struggled to attain these goals with anything less than 10 percent growth, because the old model was not generating enough jobs per unit of output. Firms increasingly replaced workers with machines embodying the latest technologies, as Chinese manufacturing moved up the value chain.

On one level, that made sense. Capital-labor substitution is at the heart of modern productivity strategies for manufacturing-based economies. But it left China in a deepening hole, as increasingly deficient in jobs per unit of output, it needed more units of output to absorb its surplus labor. Ultimately, that became more of a problem than a solution. The old manufacturing model, which fueled an unprecedented 20-fold increase in per capita income relative to the early 1990s, also sowed the seeds of excessive resource consumption and environmental degradation.

Services-led growth is, in many ways, the antidote to the "unstable, unbalanced, uncoordinated, and ultimately unsustainable" growth model. Services offer more than just a labor-intensive growth path. Compared to manufacturing, they have much smaller resource and carbon footprints. A services-led model provides China with an environmentally friendlier and ultimately more sustainable economic structure.

It is premature, of course, to conclude that a services-led transformation to slower growth is now at hand. The latest data hint at such a possibility, with the service sector expanding at what would be an annual rate of an 8.3 percent in the first quarter of this year - the third consecutive quarter of acceleration and a half-percentage point faster than the 7.8 percent first-quarter gain recorded by manufacturing and construction.

Not surprisingly, China skeptics are putting a different spin on the latest growth numbers. Fears of a shadow-bank-induced credit bubble now top the list of concerns, reinforcing longstanding concerns that China may succumb to the dreaded "middle-income trap" - a sustained growth slowdown that has ensnared most high-growth emerging economies at the juncture that China has now reached.

China is hardly immune to such a possibility. But it is unlikely to occur if China can carry out the services and consumption rebalancing that remains the core strategic initiative of its 12th Five-Year Plan (2011-15). Invariably, the middle-income trap afflicts those emerging economies that cling to early-stage development models for too long. For China, the risk will be highest if it sticks with the timeworn recipe of unbalanced manufacturing- and construction-led growth, which has created such serious sustainability problems.

If China fails to rebalance, weak external demand from a crisis-battered developed world will continue to hobble its exports, forcing it to up the ante on a credit- and investment-led growth model - in effect, doubling down on resource-intensive and environmentally damaging growth.

Financial markets, as well as growth-starved developed economies, are not thrilled with the natural rhythm of slower growth that a rebalanced Chinese economy is likely to experience, and resource industries - indeed, resource-based economies like Australia, Canada, Brazil, and Russia - have become addicted to China's old strain of unsustainable hyper-growth. Yet China knows that it is time to break that dangerous habit.

The United States is likely to have a different problem with consumer-led growth in China. After all, higher private consumption implies an end to China's surplus saving - and thus to the seemingly open-ended recycling of that surplus into dollar-based assets such as US Treasury bills. Who will then fund America's budget deficit - and on what terms?

Just as China must embrace slower growth as a natural consequence of its rebalancing imperative, the rest of the world will need to figure out how to cope when it does.

The author, a faculty member at Yale University and former Chairman of Morgan Stanley Asia, is the author of The Next Asia. Project Syndicate

(China Daily 05/03/2013 page8)

Michelle lays roses at site along Berlin Wall

Michelle lays roses at site along Berlin Wall Historic space lecture in Tiangong-1 commences

Historic space lecture in Tiangong-1 commences 'Sopranos' Star James Gandolfini dead at 51

'Sopranos' Star James Gandolfini dead at 51 UN: Number of refugees hits 18-year high

UN: Number of refugees hits 18-year high Slide: Jet exercises from aircraft carrier

Slide: Jet exercises from aircraft carrier Talks establish fishery hotline

Talks establish fishery hotline Foreign buyers eye Chinese drones

Foreign buyers eye Chinese drones UN chief hails China's peacekeepers

UN chief hails China's peacekeepers

Most Viewed

Editor's Picks

|

|

|

|

|

|

Today's Top News

Shenzhou X astronaut gives lecture today

US told to reassess duties on Chinese paper

Chinese seek greater share of satellite market

Russia rejects Obama's nuke cut proposal

US immigration bill sees Senate breakthrough

Brazilian cities revoke fare hikes

Moody's warns on China's local govt debt

Air quality in major cities drops in May

US Weekly

|

|