New growth model, new FDI scopes

Updated: 2013-05-07 08:12

By Dan Steinbock (China Daily)

|

||||||||

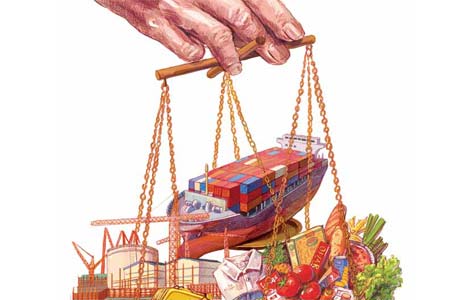

During the past three decades, China's growth was predicated on investment and net exports. In the future, it will be driven increasingly by consumption. How will the transition affect foreign companies in China? Where are their new opportunities and what are their challenges?

Last year, foreign direct investment (FDI) in China fell almost 4 percent to $112 billion, according to Ministry of Commerce data on new projects from overseas. However, central bank data offer a bullish picture of reinvested earnings from foreign companies already operating on the Chinese mainland.

Today, China is the world's top destination for FDI, as the United Nations data attest. But as China is changing, so will FDI.

Initially, many foreign multinationals in China came to benefit from low price and low costs. They used China primarily as an export platform. Today, multinationals are expanding their operations in China to take advantage of market access.

As China's growth model will gradually shift from investment and net exports to consumption, it is likely to become one of the fastest-growing consumer markets in the world.

In the past, big multinational consulting companies, including McKinsey, Boston Consulting Group, AT Kearney and Booz Allen Hamilton, promoted China as the world factory. For a few years now, they have shifted the spotlight to China's middle class, consumption engine and demand locomotive.

Today, China is the world's largest and favorite FDI destination because it is seen as the world's largest marketplace of the future.

By 2015, Ford Motor hopes to double its retail and production capacity in China. Like earlier in America, it is investing productive capital and creating good jobs, which will now provide livelihood to ordinary Chinese and thus give them the opportunity to consume - which, in turn, will expand the middle class and consumption in China.

These investments reflect the ongoing new deal of foreign investment in China. In the past, investments were focused on the first- and second-tier cities in the prosperous coastal regions. Today, they are also shifting to other regions.

As industrial producers - from US-based Dover to German chemical producer BASF - are no longer growing as fast as in the past, China is becoming the destination market for foreign consumer and services groups hoping to benefit from the rapidly rising domestic demand.

For more than a century, Procter & Gamble, the consumer goods leader, focused on developing household staples for the expanding American middle class. Over the past few years, however, the squeeze on middle-class America has taught it to look for new growth markets, including China's nascent middle class.

China's service industries will need a local workforce that knows the market intimately. Consequently, the world's largest advertisers, marketers and advertising agency networks are boosting their operations in China. "We have some plans for developing WPP in a different form in China, more locally based," says Martin Sorrell, CEO of WPP, the world's largest advertising company. Like other senior executives, Sorrell expects localization to foster an even stronger position.

In 2011, FDI flows into the Chinese mainland and Hong Kong reached a historic high of $124 billion and $83 billion. While FDI in manufacturing on the mainland has stagnated, the service sector's share in FDI has exceeded that in manufacturing, for the first time.

As China moves higher in the value-added chain, it is no longer just the mecca of assembly plants for foreign producers. It is also becoming the global center of innovation. Throughout the 1950s and 1960s, the US enjoyed superior leadership in science and technology, research and development, and patents. Since the late 1970s and 1980s, the innovative capacities of the US, Western Europe and Japan have converged.

Last year, the global patent power shifted from the US to China, and the global R&D power will migrate to China probably within a decade. In the US, patents are dominated by multinational giants, including Qualcomm, IBM, Hewlett-Packard, 3M, Procter & Gamble, Microsoft, Dupont and Intel. They do not just represent computer technologies, medical sciences, pharmaceuticals, energy and digital communication. They also epitomize major foreign investors on the mainland.

From the standpoint of foreign companies operating in China, these changes require a U-turn in perspective. While the latter is understood by informed large multinationals, many small and medium-size enterprises understand poorly the new opportunities in China. As the full implications of China's growth transition and the associated FDI shifts become more familiar, the repercussions will reverberate regionally and worldwide.

Imagine the US (population 316 million), plus Europe's 27 member states (502 million), plus Japan (127 million), coupled with Brazil (200 million) Russia (143 million), and Ethiopia (84 million). Then imagine a track record of past growth and solid growth potential in the future, including a Chinese dream with a rising middle class and soaring consumer demand. That's what drives multinational FDI in China today.

The author is research director of international business at India, China and America Institute (US) and visiting fellow at Shanghai Institutes for International Studies (China) and EU Centre (Singapore).

Michelle lays roses at site along Berlin Wall

Michelle lays roses at site along Berlin Wall Historic space lecture in Tiangong-1 commences

Historic space lecture in Tiangong-1 commences 'Sopranos' Star James Gandolfini dead at 51

'Sopranos' Star James Gandolfini dead at 51 UN: Number of refugees hits 18-year high

UN: Number of refugees hits 18-year high Slide: Jet exercises from aircraft carrier

Slide: Jet exercises from aircraft carrier Talks establish fishery hotline

Talks establish fishery hotline Foreign buyers eye Chinese drones

Foreign buyers eye Chinese drones UN chief hails China's peacekeepers

UN chief hails China's peacekeepers

Most Viewed

Editor's Picks

|

|

|

|

|

|

Today's Top News

Shenzhou X astronaut gives lecture today

US told to reassess duties on Chinese paper

Chinese seek greater share of satellite market

Russia rejects Obama's nuke cut proposal

US immigration bill sees Senate breakthrough

Brazilian cities revoke fare hikes

Moody's warns on China's local govt debt

Air quality in major cities drops in May

US Weekly

|

|