Avoiding failure in the world of corporate business

Updated: 2013-06-17 07:36

(China Daily)

|

||||||||

Management | Zheng Yangpeng

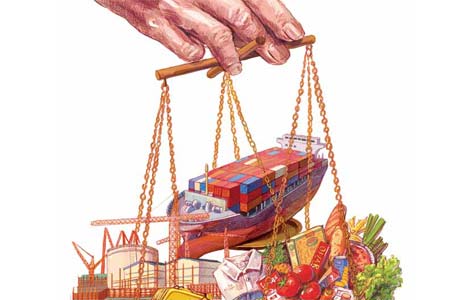

There is no shortage of reflections on the market failure in the West after the 2008 financial crisis, with many observers regarding what Yi Zhihong, dean of the Business School of Renmin University of China, described as "the supremacy of shareholder interest" being the main culprit. But the book Firm Commitment: Why the Corporation is Failing Us and How to Restore Trust in It by Colin Mayer, a professor of management studies at the University of Oxford's Said Business School, is not just another fashionable tome on the topic. Rather, it is a solemn contemplation of the roots of corporations' defects.

You can sense the seriousness of his thoughts in every line. According to him, the book is both a "tribute and a condemnation" of this "remarkable institution that has created more prosperity and misery than could have been imagined".

When interviewed by China Daily, the academic said the 2008 financial crisis was not the main factor that prompted him to write the book. Rather, it was a distillation of his years of consistent research and on-site experience on the subject. His focus saw a few shifts, from corporate finance to corporate ownership and control, from corporate contracts to financial regulation.

These led to his conclusion that corporations fail us primarily because their institutional emphasis is in the interests of short-term stock market speculators, rather than other stakeholders, including customers, suppliers, employees and the community in which it is located.

As early as 2006 he was due to deliver the manuscript of the book to Oxford University Press but he failed to because he became dean of the Said Business School that year. He finally found time to finish the book when he quit the post in 2011.

According to him, a fundamental failure is a confusion about the purpose and meaning of a corporation. The nature of a corporation does not derive from a simple relation between input and output or lower costs of transaction. Its first and foremost objective should not be to its shareholders or to its stakeholders. It is to make, develop and deliver things and to service people, communities and nations. It does this through engaging investors and stakeholders and it assumes a variety of forms to achieve this, of which the traditional model - the shareholder-oriented corporation - is one, but only one, manifestation.

The shareholder-oriented corporation, according to him, gives a shareholder for three days as many rights in that period as the long-term investor, "as if we are conferring voting rights on members of the population who intend to renounce their citizenship tomorrow".

It is also a system in which hostile takeovers can too easily destroy jobs, markets and ethics in long-established companies. A counter example Mayer likes to cite is Rolls-Royce Plc. The British aircraft engine manufacturer, one of the few remaining large manufacturers in Britain, managed to survive because the government retains a "golden share" in it, giving it a veto over change and control of the corporation. Had that golden share not existed, in all probability it would go the way many other British corporations suffered, going bankrupt or being taken over by foreign investors, Mayer said.

At first glance, Mayer's reasoning is reminiscent of the corporate social responsibility or corporate citizenship theories that prevailed in those years. But Mayer said he actually was "quite critical" about those ideas. He said although in principle they sound quite appealing, in practice they are not well applied, in particular when corporations found themselves in financial difficulties or economic condition got worse. They became very willing to give up the practice in favor of traditional profit-maximizing objectives.

"So CSR has in practice turned out to be what in English we describe as a 'fair weather' principle: as long as it is sunny and things go well, it is relatively easy to make CSR commitments. But when the clouds, rain and storms come, they get rid of those principles," Mayer said.

What can China learn from Mayer's book, deeply rooted in the West as it is?

Mayer's answer, to put it simply, is China should avoid the faults made by the West. A Western corporation style does not need to be blindly pursued. Credible long-term investors should be incorporated to ensure a corporation's long-term prosperity. However, the question is, who or what can take the place of the State as a long-term investor?

Mayer said there are many options, including many financial institutions such as pension and insurance funds. The problem in China, however, is that pension funds have the direct or indirect involvement of the State. But he added that "there is no reason" not to incorporate foreign private pension funds as co-investors to counterbalance the influence of the State. In South Korea, for example, the National Pension Scheme is an owner of the chaebol, a form of business conglomerate.

Mayer said although State operations always mean low efficiency, privatization is not a one-size-fits-all solution either. Britain's history provided considerable experience in this respect.

"Britain's privatization of the railways has not been a happy experience at all," Mayer said. "Many people question whether the privatization of the railways actually delivered any benefits because they did not see a clear and great improvement in efficiency. What is quite clear though is there has been a substantial increase in ticket prices."

In Britain, the railways were initially, as they were in China, administered by the government. They then became state-owned enterprises before, after the late Margaret Thatcher's premiership from 1979 to 1990, being fully privatized and sold off. Not only the trains but also the tracks were privatized. Railtrack behaved like many a private commercial company, cutting costs where it could, including maintenance fees. After two serious accidents occurred, Railtrack was taken out of straightforward private ownership and became mutually owned by a number of interested parties. In many respects it is considered to be the least successful privatization program in Britain.

According to Mayer, the lack of success partly lies in the nature of the sector: It is very difficult to introduce competition in the railway sector because trains are run on a limited number of tracks. In contrast, it is relatively easy to introduce competition in the airline sector. Allowing state-owned airlines to compete with private airlines proved to be beneficial to customers. For example, competition forced British Airways, a state-owned enterprise to become a very successful company.

Contact the writer at zhengyangpeng@chinadaily.com.cn

(China Daily 06/17/2013 page20)

Michelle lays roses at site along Berlin Wall

Michelle lays roses at site along Berlin Wall Historic space lecture in Tiangong-1 commences

Historic space lecture in Tiangong-1 commences 'Sopranos' Star James Gandolfini dead at 51

'Sopranos' Star James Gandolfini dead at 51 UN: Number of refugees hits 18-year high

UN: Number of refugees hits 18-year high Slide: Jet exercises from aircraft carrier

Slide: Jet exercises from aircraft carrier Talks establish fishery hotline

Talks establish fishery hotline Foreign buyers eye Chinese drones

Foreign buyers eye Chinese drones UN chief hails China's peacekeepers

UN chief hails China's peacekeepers

Most Viewed

Editor's Picks

|

|

|

|

|

|

Today's Top News

Shenzhou X astronaut gives lecture today

US told to reassess duties on Chinese paper

Chinese seek greater share of satellite market

Russia rejects Obama's nuke cut proposal

US immigration bill sees Senate breakthrough

Brazilian cities revoke fare hikes

Moody's warns on China's local govt debt

Air quality in major cities drops in May

US Weekly

|

|