China's financial might takes shape

Updated: 2013-03-08 07:10

By John Ross (China Daily)

|

||||||||

Before long the chinese will dominate list of 100 top influential people in finance

The US magazine Worth published a report recently analyzing the 100 most powerful people in global finance. Four were from China: Shang Fulin, chairman of the China Banking Regulatory Commission; Zhou Xiaochuan, governor of the People's Bank of China; Lou Jiwei, chairman and CEO of China Investment Corp; and Jiang Jianqing, chairman of the Industrial and Commercial Bank of China. They were ranked 14th, 15th, 27th and 31st.

That only four of China's top financial figures were included in the list shows how much understanding of the power of China's financial and banking system still lags behind its reality.

To grasp the underlying dynamic of the global financial industry it should be noted that it is a mistake to understand the strength of China's economy by statistics (such as the facts that China produces as much steel as the next 38 countries combined; more cement than the rest of the world put together; that it is the world's largest market for TVs, refrigerators, mobile phones, cars; or that it has more than twice as many Internet users as the US).

These figures are impressive but far from illustrate the real core of China's economic power. The real center of its economic strength, which determines both its domestic and global expansion, is unparalleled financial strength.

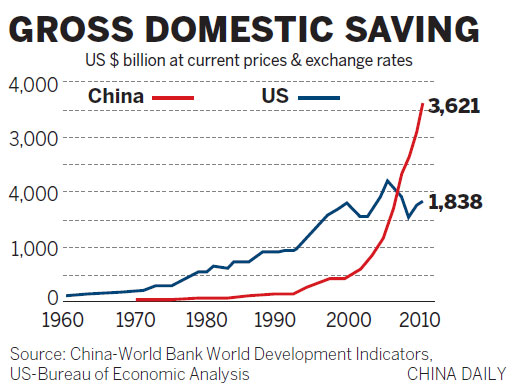

China has yet to overtake the US in GDP, but the annual sum of China's finance available for global or domestic investment - its savings - is already twice that of the US. As the chart shows, China's savings in 2011, the last year for which comprehensive figures are available, were $3.6 trillion (2.8 trillion euros), double that in the US.

But savings are the raw material of the financial system. It is this huge flow passing through China's banking system that is making China the world's financial superpower. China's $3.3 trillion foreign exchange reserves, easily the world's largest, are a powerful adjunct but it is the year-after-year generation of domestic finance on a scale that has no international parallel which is the unmatched core of China's economic strength.

To see the dynamic this is creating in the global finance industry it is useful to compare the main indices for banks in China and the US. When this year's figures are published they will further reinforce these trends.

US banks reporting last year were still ahead of China's on revenue - $550 billion compared with $404 billion, and on assets - $10,079 billion compared with $9,895 billion. But on profits China's banks had already overtaken their US competitors, $105 billion compared with $68 billion. China's banks also held the lead in stock market valuation, $992 billion to $847 billion.

At the beginning of this year, both China (ICBC, China Construction Bank, Agricultural Bank of China, Bank of China), and the US (Wells Fargo, JPMorgan Chase, Citigroup, Bank of America) had four out of the world's top 10 banks by market capitalization. But the total valuation of the Chinese banks was $706 billion compared with $620 billion. ICBC is the world's largest bank by both profit and capitalization.

In other financial fields - insurance, mortgage lenders and credit cards - the US still maintains a lead over China. But in core banking strength there is essentially no difference between China and the US.

But by every indicator the rate of growth of China's banks is many times higher than that of their US competitors. By revenue China's banks were 16 percent as large as US banks in 2007, and by last year they were 74 percent as large. By assets the corresponding figures were 30 percent and 98 percent, by market valuation 43 percent and 117 percent, and by profit 17 percent and 155 percent.

China's far more rapid buildup of domestic finance means that the balance will progressively and rapidly move in favor of its institutions. So before long China's banks will overtake US banks on all measures. China's underlying financial strength is rapidly being transformed into institutional strength in its banking system.

Where US banks traditionally held a strong lead over China is that China's were essentially domestic banks but US banks operated globally. However, this is beginning to change as China's banks go global.

First to globalize were China's development banks. During 2005 and 2011 China Development Bank and Export-Import Bank of China provided more than $75 billion in loan commitments to Latin America.

But now globalization of China's commercial banks is proceeding rapidly. By the beginning of this year, ICBC operated in 39 countries with overseas assets of $170 billion, a 30 percent increase on 2011. The stability and state guarantee of China's banks is attractive compared with the continued scandals from US and European competitors, making it clear that developing the necessary management skills is now the primary difficulty in expanding China's banks' overseas operations.

China's banks have so far concentrated on developing countries. For example, key acquisitions were ICBC's purchase of a 20 percent stake in Standard Bank, South Africa and Africa's largest bank. The advantage of the combination of Standard Bank's local knowledge throughout Africa and ICBC's huge financial firepower is evident. ICBC's shareholding in South Africa Standard Bank also made it easy to buy Standard Bank's Argentinian subsidiary, consolidating ICBC's position in Latin America.

But the financial strength of China's banks gives them the opportunity to directly expand operations in developed economies.

Last year ICBC carried out China's first takeover of a US bank with Bank of East Asia. The international expansion of yuan operations - with the world's largest foreign exchange dealing center, London, trying to compete as an offshore operator with Hong Kong and Singapore - centrally involves China's banks.

Globalization of China's banks cannot be instantaneous. But the problems involved are time in acquiring permits, training management, creating infrastructure and other things, rather than fundamental financial strength. Overcoming these difficulties, given the unparalleled financial muscle that can be applied, is simply a matter of time.

How should the situation be summarized? It is sometimes assumed manufacturing is China's strongest industry. This is a mistake. China is the world's largest manufacturer and largest manufacturing exporter. But a substantial part of China's manufacturing output, and half its exports, are still by foreign companies. It will take significant time to build the power of China's own manufacturing companies. But the foundations of China's banks are already those of an emerging financial superpower. It is only a matter of time, a rather short one, before that translates into an equivalent strength of China's global finance companies.

Within a decade a list of the 100 most influential people in world finance will not contain four from China. It is likely to be dominated by figures from China.

The author is a senior fellow at Chongyang Institute for Financial Studies, Renmin University of China, and former director of economic and business policy for the mayor of London. The views do not necessarily reflect those of China Daily.

(China Daily 03/08/2013 page9)

Li Na on Time cover, makes influential 100 list

Li Na on Time cover, makes influential 100 list FBI releases photos of 2 Boston bombings suspects

FBI releases photos of 2 Boston bombings suspects World's wackiest hairstyles

World's wackiest hairstyles Sandstorms strike Northwest China

Sandstorms strike Northwest China Never-seen photos of Madonna on display

Never-seen photos of Madonna on display H7N9 outbreak linked to waterfowl migration

H7N9 outbreak linked to waterfowl migration Dozens feared dead in Texas plant blast

Dozens feared dead in Texas plant blast Venezuelan court rules out manual votes counting

Venezuelan court rules out manual votes counting

Most Viewed

Editor's Picks

|

|

|

|

|

|

Today's Top News

Boston bombing suspect reported cornered on boat

7.0-magnitude quake hits Sichuan

Cross-talk artist helps to spread the word

'Green' awareness levels drop in Beijing

Palace Museum spruces up

First couple on Time's list of most influential

H7N9 flu transmission studied

Trading channels 'need to broaden'

US Weekly

|

|