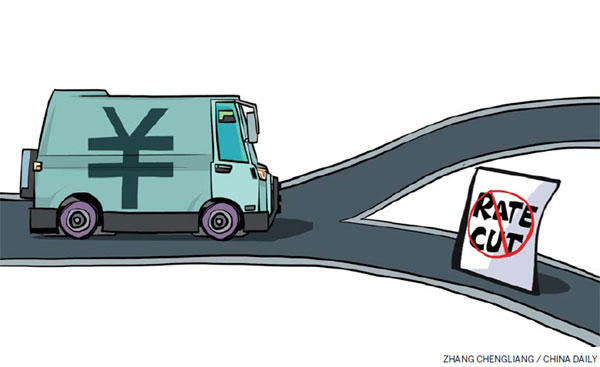

Why rates can stay on hold

Updated: 2013-05-24 08:50

By Zhou Feng (China Daily)

|

||||||||

China's economic growth may continue to slow but there's no pressing need to pump it up

Whenever the Chinese economy slows down, there are calls to trim the interest rate to shore up growth. So it is no surprise to see such appeals growing in recent months.

Gross domestic product grew 7.7 percent in the first quarter, down from 7.9 percent in the final quarter of last year. That drip seems to justify the need for greater liquidity and cheap lending.

Supporters of the rate cut also have other reasons. Inflation, described as an uncaged tiger by former premier Wen Jiabao, is mild, leaving room for policymakers to reduce interest rates.

China's inflation rate, measured by the consumer price index, stood at 2.4 percent year-on-year in April. Although it was up from 2.1 percent in March, the rate was much lower than the 3.2 percent in February and well below the year's target of 3.5 percent. Going on experience, if the rate is lower than 3 percent for two consecutive months, top policymakers deem inflationary pressure mild, and will be bold in using rate moves.

Advocates for a rate reduction have another reason - massive inflows of hot money show the urgent need for a rate cut that could help quell international speculation in the yuan.

For years, China and the world's other major economies have been poles apart in their interest rates, with China's being much higher. That difference widened recently after major economies either further lowered interest rates or initiated quantitative easing. Cuts by South Korea, Australia and India have been reported this month.

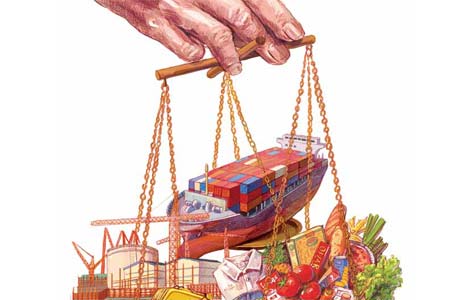

That creates room for speculators to arbitrage and has ushered a large amount of international capital into China. The yuan's fast appreciation in recent months has given rise to the trend. The massive capital inflows are reflected in the latest trade and monetary figures.

China's foreign trade has grown much faster than expected this year. The country's trade with markets that serve as international capital's proxies to China increased exceptionally fast, partly because hot money is flowing in under the guise of trade.

If trade figures are not enough to reflect the capital inflows, foreign exchange purchase figures are.

The central bank and commercial lenders have been net foreign exchange purchasers over the past five months, suggesting that money is continuing to flow into the country. Banks brought in nearly 1.2 trillion yuan ($196 billion) worth of foreign exchange in the first quarter on a net basis, the highest in recent years.

Amid the inflow pressure, some people argue that a rate cut is needed to narrow the interest margin so that speculative international money can leave China.

But does China need to follow the international trend and cut its interest rate?

I would say no.

First of all, an interest rate cut is not necessarily a cure for economic slowdown, especially given the fact that this round of economic sluggishness is mainly due to a structural change instead of a shortage of liquidity or lack of cheap lending.

The Chinese economy is not growing as robustly as it was, but that is basically a result of its structural transition under both domestic and external pressures. Within China, the authorities are curbing the growth of property prices to squeeze asset bubbles and improve the real economy. Externally, weak global demand is forcing the country to cut its reliance on exports. Under these circumstances, economic slowdown is inevitable, and is not caused by a lack of liquidity.

Indeed, growth of M2, the broad measure of money supply that covers cash in circulation and all deposits, had increased to 16.1 percent by the end of April, 0.4 percentage point higher than March. That was higher than the annual growth limit of 13 percent for the indicator, which the central bank had set earlier.

In addition, total social financing, an index that covers all loans, bond issuance and stock sales, stood at 1.75 trillion yuan in April, higher than the market forecast of 1.5 trillion yuan.

These figures all reflect that China is not short of money supply. In fact, lending is excessive and has already resulted in growing bad debts. According to the China Banking Regulatory Commission, outstanding non-performing loans stood at 526.5 billion yuan, up by 33.6 billion yuan from the end of 2012, while the ratio of bad loans to total lending rose by 0.01 percentage point to 0.96 percent during the first quarter of the year.

There is no need to encourage lending by lowering the rate. What policymakers need to do is to improve the structure of lending; that is, allow more funding to private companies and the real economy. Despite growing liquidity, lending to private companies and small and medium-sized enterprises is not growing accordingly. In the first quarter of the year, nearly 64 percent of social finance went to state companies and government projects. That was 4 percentage points higher than the previous quarter.

Given that the public sector is usually less efficient than the private sector, the quality of lending is not high. Also, as the private sector employs more workers, less lending to the sector may ultimately lower the employment rate and adversely affect people's consumption habits, a scenario policymakers do not want to see.

In this sense, it is the lending structure, rather than the lending amount, that deserves more attention, and the need to cut the interest rate would not seem that pressing. So is China really free from any inflationary threat to accommodate an interest rate cut?

Given the abundant liquidity, the inflation bomb threat has not been totally defused. Indeed, inflation may rise with the prediction that food prices will peak in six months. Due to seasonal and cyclical effects, prices of a number of major food items such as pork are likely to rise remarkably in about six months. Food accounts for one-third of China's CPI.

If the interest rate is cut now, its effect on liquidity will fully surface in about three to six months, overlapping the time when food price pressure becomes evident.

The two happening at the same time will make inflation a big issue.

As for hot money inflows, a rate cut will help squeeze some international speculative capital out of the Chinese market. But the side effect of an interest rate cut will be more severe than international money inflow.

Compared with money supplies circulating within the domestic system, money coming from outside China is not large. If the interest rate is reduced, an increase in liquidity within the domestic system will outweigh the foreign capital leaving China. Overall, liquidity will increase even more. That does not help improve the bigger picture.

The author is a financial analyst in Shanghai. The views do not necessarily reflect those of China Daily. He can be reached at michaelzhoufeng@gmail.com

(China Daily 05/24/2013 page8)

Michelle lays roses at site along Berlin Wall

Michelle lays roses at site along Berlin Wall Historic space lecture in Tiangong-1 commences

Historic space lecture in Tiangong-1 commences 'Sopranos' Star James Gandolfini dead at 51

'Sopranos' Star James Gandolfini dead at 51 UN: Number of refugees hits 18-year high

UN: Number of refugees hits 18-year high Slide: Jet exercises from aircraft carrier

Slide: Jet exercises from aircraft carrier Talks establish fishery hotline

Talks establish fishery hotline Foreign buyers eye Chinese drones

Foreign buyers eye Chinese drones UN chief hails China's peacekeepers

UN chief hails China's peacekeepers

Most Viewed

Editor's Picks

|

|

|

|

|

|

Today's Top News

Shenzhou X astronaut gives lecture today

US told to reassess duties on Chinese paper

Chinese seek greater share of satellite market

Russia rejects Obama's nuke cut proposal

US immigration bill sees Senate breakthrough

Brazilian cities revoke fare hikes

Moody's warns on China's local govt debt

Air quality in major cities drops in May

US Weekly

|

|