Shipyards battling to stay afloat

Updated: 2013-05-24 08:51

By Alfred Romann (China Daily)

|

||||||||

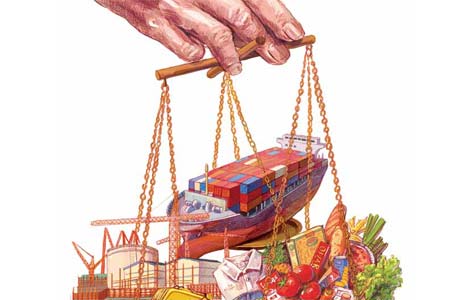

Chinese shipyards have powered ahead and now produce more ships than anybody else, but the business of shipbuilding is becoming increasingly difficult and profits harder to come by.

Although still major players and the world's biggest tanker producers, South Korean mega-yards no longer dominate every sector of the market. China is making more bulk carriers than any other ship producer in the world and Japan is also making a comeback, partly spurred by a lower yen, which makes it an attractive market for ship buyers.

"Who still leads the pack? Well, it's China," says Martin Rowe, managing director of Clarkson Asia Ltd.

China's output of ships in 2012 was close to 20 million compensated gross tons, an indicator of the amount of work that goes into building a ship.

The nation's shipbuilding industry is extremely diversified, with 153 shipyards in operation.

In South Korea, the No 2 player, production is concentrated in just four or five "super-yards" that dominate the industry.

But the business of shipbuilding is changing rapidly, along with a shipping industry that has gone from massive boom to historic bust in less than half a decade. Through 2012, around 220 yards around the world were taking orders for ships, each holding at least one contract, less than half the number in 2007 or 2008.

"A vast number of yards, particularly in China, have either been mothballed, keeping the facilities running without producing anything, or have gone into liquidation," says Rowe.

The boom days of 2008 and 2009, when new-ship orders skyrocketed, have come and gone. Although the number of ships ordered around the world in the first couple of months of this year was surprisingly high for an industry trying to deal with overcapacity, the orders were anything but uniform.

The top yard in China by order book is Jiangsu Rongsheng Heavy Industries Co, which builds bulk carriers, ore carriers, oil tankers, and a variety of other vessels. Despite the country's position as the world's leading shipbuilder, the company has faced difficult times during the last year. In 2012, revenue at its Hong Kong listed arm in 2012 dropped to half of the 2011 figure, and the company posted a net loss for the year.

High fuel costs, environmental concerns and regulations mean that shipyards have to be creative. Many build ships at a loss today.

Financing is another issue because money for ships has dried up, with banks less willing to invest given the state of the industry. In 2005, the charter rate of some ships amounted to about three times the cost of the fuel. Today, the cost of fuel can be double the time-charter price of a ship, a result of increases in the cost of fuel and massive declines in shipping rates.

The price of a barrel of oil is now more than 40 percent higher than in 2005, while shipping rates have plummeted in the past three years to levels last seen in 1997. A Capesize vessel - a designation for ships too large to use the Suez canal and which therefore have to round the Cape of Good Hope or Cape Horn - that would have fetched an average rate of $35,300 (27,477 euros) through 2009, fetched $11,700 last year.

And a slew of new factors are likely to come into play to make things even more difficult. These include a series of new regulations, mostly environmental, that will kick in through 2025.

The good news for shipbuilders is that turnover is rising. A ship's traditional 25-year lifespan, or number of years in use, is being reduced by roughly 10 years in some cases, as owners try to economize and add newer and more efficient ships to their fleets.

For China Daily

(China Daily 05/24/2013 page11)

Michelle lays roses at site along Berlin Wall

Michelle lays roses at site along Berlin Wall Historic space lecture in Tiangong-1 commences

Historic space lecture in Tiangong-1 commences 'Sopranos' Star James Gandolfini dead at 51

'Sopranos' Star James Gandolfini dead at 51 UN: Number of refugees hits 18-year high

UN: Number of refugees hits 18-year high Slide: Jet exercises from aircraft carrier

Slide: Jet exercises from aircraft carrier Talks establish fishery hotline

Talks establish fishery hotline Foreign buyers eye Chinese drones

Foreign buyers eye Chinese drones UN chief hails China's peacekeepers

UN chief hails China's peacekeepers

Most Viewed

Editor's Picks

|

|

|

|

|

|

Today's Top News

Shenzhou X astronaut gives lecture today

US told to reassess duties on Chinese paper

Chinese seek greater share of satellite market

Russia rejects Obama's nuke cut proposal

US immigration bill sees Senate breakthrough

Brazilian cities revoke fare hikes

Moody's warns on China's local govt debt

Air quality in major cities drops in May

US Weekly

|

|