EU summit to deal with crisis

Updated: 2012-06-25 07:53

By AFP in Brussels (China Daily)

|

||||||||

Europe's leaders gather for an important summit this week under intense global pressure to head off a potentially catastrophic economic collapse.

Months ago, European Union President Herman Van Rompuy said in off-the-cuff remarks that the eurozone stood "back to the wall", "at the edge of a cliff", "with a knife at its throat".

That was before the relentless two-year sovereign debt crisis wrecking much of Europe hit the unthinkable - infecting Spain, the eurozone's fourth-largest economy, and threatening Italy, its third-largest, after earlier rescues of Greece, Ireland and Portugal.

"An unwinding of the eurozone... would be the defining crisis of the entire century. It would be a catastrophe," Yves Tiberghien, of the University of British Columbia, said after this week's G20 talks in Mexico.

"They created this great experiment," he said of the 10-year-old single currency shared by 17 vastly disparate nations.

"It was very daring but we know now it's incomplete. It's very dangerous. It doesn't work It's not functional to do monetary union without banking union and fiscal union and therefore higher political integration."

At the summit - to be held on Thursday and Friday in Brussels - the slight and canny Van Rompuy, a former Belgian premier, will attempt to take the eurozone up that road.

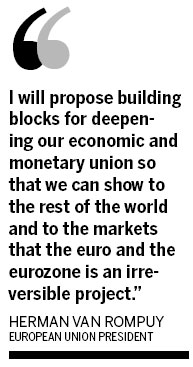

"I will propose building blocks for deepening our economic and monetary union so that we can show to the rest of the world and to the markets that the euro and the eurozone is an irreversible project," he told G20 leaders.

The EU's first moves would be to initiate growth and integrate Europe's banking sector, he said.

At talks between the eurozone's Big Four in Rome last Friday, leaders of Germany, France, Italy and Spain agreed to inject up to 130 billion euros ($163 billion) - 1 percent of European gross domestic product - into giant infrastructure projects able to provide jobs at a time when one in four young people is unemployed in some nations.

The lesson of the crisis, said German Chancellor Angela Merkel, was "more Europe, not less Europe".

"We need to work more closely together politically, especially in the eurozone. Whoever has a common currency must also have coherent policies. That is also a lesson from the last two years," she said.

Powerhouse Germany favors common taxation and budget policies - which would require treaty change - but is reluctant to share debt, unlike its traditional core EU partner France, which favors creating eurobonds.

At the Brussels summit, the first of Van Rompuy's "building blocks" is expected to be a proposal for a banking union, should he clinch a tough-to-reach compromise over the role of the European Central Bank.

"Banking union is a fundamental element," he told German paper Welt am Sonntag, in an interview published on Sunday.

"I think we can move forward there more quickly than in other areas."

Banking union would be a first step in a long-term - perhaps decade-long - roadmap to political union to be outlined to EU leaders by Van Rompuy, with dates and institutional problems such as treaty change set out by the year-end.

EU diplomats said Van Rompuy had been asked to ready a detailed proposal for October or possibly December.

But a move toward Europe-wide guarantees on deposits and a central authority to close bad banks would both boost confidence and ease the flow of cash.

"Out of the chaos are emerging ideas," said a senior EU diplomat. "It will be a political union at the end of the day."

In a reminder that this week's get-together will be of special importance, US President Barack Obama said last week: "I am confident that, over the next several weeks, Europe will paint a picture of where we need to go."

Adding to the pressure, International Monetary Fund chief Christine Lagarde said on Friday that "a determined and forceful move toward a complete European monetary union should be reaffirmed in order to restore faith in the system".

In the meantime, the IMF is leaning on a reluctant Merkel to allow the eurozone's rescue fund, the European Financial Stability Facility, to lend directly to Spain's distressed banks rather than to the government.

This is in order to break a so-called "feedback loop", in which sovereigns face mounting borrowing costs when forced to help their own banks, leading to a vicious circle of mounting debt weighing on all institutions.

Spain will formally request a eurozone loan for its banks on Monday.

The "men in black" inspectors from the IMF, ECB and European Commission return to Athens on Monday to check the state of play on reforms pledged in exchange for a 130-billion-euro loan.

The new coalition government formed last week, backed by conservative, socialist and moderate leftist parties, wants the austerity-heavy terms of Greece's bailout tweaked to kick-start growth.

(China Daily 06/25/2012 page14)

Relief reaches isolated village

Relief reaches isolated village Rainfall poses new threats to quake-hit region

Rainfall poses new threats to quake-hit region Funerals begin for Boston bombing victims

Funerals begin for Boston bombing victims Quake takeaway from China's Air Force

Quake takeaway from China's Air Force Obama celebrates young inventors at science fair

Obama celebrates young inventors at science fair Earth Day marked around the world

Earth Day marked around the world Volunteer team helping students find sense of normalcy

Volunteer team helping students find sense of normalcy Ethnic groups quick to join rescue efforts

Ethnic groups quick to join rescue efforts

Most Viewed

Editor's Picks

|

|

|

|

|

|

Today's Top News

Health new priority for quake zone

Xi meets US top military officer

Japan's boats driven out of Diaoyu

China mulls online shopping legislation

Bird flu death toll rises to 22

Putin appoints new ambassador to China

Japanese ships blocked from Diaoyu Islands

Inspired by Guan, more Chinese pick up golf

US Weekly

|

|