Getting out of the hole

Updated: 2012-06-15 09:27

By Joseph Boris (China Daily)

|

||||||||

Ample opportunities in US Stock market for Chinese firms with good fundamentals, experts say

Though Chinese companies which are publicly traded and have stock issues in US stock exchanges are facing rough weather in the US on a host of issues like accounting standards and financial disclosures, there are still ample opportunities for companies with good fundamentals, experts say.

Many US investors have shunned the bad Chinese apples, but some also say the good apples have also been caught in the crossfire. The spate of such incidents have also led to calls for tough actions against the Chinese companies that violate US listing rules.

|

Related readings: |

Though most of the listing problems center on the differing accounting standards practiced by the Chinese companies vis-a-vis global practices, there have also been instances of companies avoiding the stringent US listing regulations by using the now-famous "reverse merger" process and in some cases wrong financial disclosures.

In reality the compound effect of all these actions has been the steady erosion of investor confidence and a massive sell-off of Chinese equities on the US stock exchanges. Several lawsuits have also been filed against Chinese companies in US courts.

The robust pipeline of Chinese initial public offerings in the US has also been crimped badly due to the uncertain market conditions. This year, only one company has floated its shares in the US so far, compared with over 13 listings in 2011.

The bleak situation has also prompted several prospective IPO candidates like China Auto Rental Holdings Inc to develop cold feet on listing. The Guangzhou-based car-rental company said on April 25 that it had deferred its plan to raise $137.5 million on the Nasdaq, citing the current unfavorable capital market conditions.

Crocker Coulson, president of CCG Investor Relations in New York and an adviser to several Chinese companies planning to list their shares on US stock exchanges, feels that the "bad actors" are setting a bad precedent for the others.

"They have abused the trust and stolen from shareholders", making it hard - and in some cases impossible - for legitimate, well-run Chinese issuers to get a fair value for the securities listed abroad, he says.

The few rotten-apples-spoiling-the-bunch argument has also been cited in public complaints by some of the accused Chinese companies. According to the Chinese companies, most of the SEC allegations are rather exaggerated and unfounded and smack of an overall negative sentiment against them.

"What everyone has been saying is the same as what was being said before. You need better auditors and a better understanding of what has to be done to prepare for a US listing," says Robert Schechter, managing director of Dragon Gate Investment Partners in New York, which has acted as an adviser to Chinese companies seeking US listing.

|

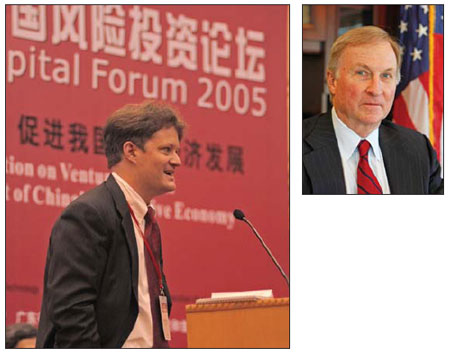

Left: Crocker Coulson, president of CCG Investor Relations in New York. Right: James Doty, chairman of the US Public Company Accounting Oversight Board. Provided to China Daily |

Continuing impasse

At the heart of this whole imbroglio is the lack of clear understanding between the two sides on what really needs to be done, Schechter says.

James Doty, chairman of the US Public Company Accounting Oversight Board said in March that his agency and the SEC were unable to inspect US-listed companies from China and other countries "due to asserted restrictions under local law or objections based on the national sovereignty".

But on May 8, after talks in Beijing, Doty said he expects US inspectors to be roped in as observers during the inspection of audit firms that Chinese regulators are planning this fall. The observations "will be a first step toward greater cooperation on cross-border oversight and joint inspections," he said. However, he added, "One can never guarantee the outcome of this."

Stock market regulators in Hong Kong have indicated that they would hold the auditors accountable for false statements made by the Chinese corporate clients that are listed on HK stock exchanges.

But in a move that may further complicate the chances of a smooth resolution, China in May unveiled rules calling for Chinese partners to be in control of the day-to-day operations at the local operations of the Big Four accounting firms - Ernst & Young, KPMG, Deloitte Touche Tohmatsu and PricewaterhouseCoopers.

Though this kind of arrangement is similar to how the accounting industry works in other countries, many Western investors remain skeptical, as they believe the move undermines the credibility of these firms in China.

Resolving the audit-cooperation issue takes on added urgency considering that Chinese authorities generally maintain sole control over the information that auditors have on domestic companies. If there were no resolution, it would make it even tougher for US regulators to share their oversight and findings especially when investigating claims of accounting fraud. Another fallout of such an action would be the debarment of Chinese auditors from working for companies trading in the US.

A possible foretaste of the even harder-line US action came on May 9, the day before China came out with its audit-localization rule change. The SEC sued Deloitte affiliate D&T Shanghai over its refusal to surrender documents involving a Deloitte client under SEC investigation. Deloitte cited strict Chinese state-secrecy laws for its stance, which the SEC said violates the Sarbanes-Oxley law on foreign public accounting firms' work for issuers of US-traded securities.

Cross-border differences

Some China-based, US-listed companies that have come under the SEC lens have said that most of the investigations have been triggered by the short-sellers who were unable to make profits. In "shorting", a trader always borrows shares of a company with the intention of returning them later to the borrower at a profit if their price goes down.

Violet Ho, a certified fraud examiner based in Hong Kong with corporate-intelligence firm Kroll Advisory Solutions, says there is an "us-versus-them kind of distrust on both sides". The US investors and regulators should be wary of treating every misstep by Chinese companies as the evidence of scandal, she says.

"There are a lot of issues at stake; it's definitely not simplistic," she said. "I think what has happened over last 18 months is a vicious cycle. The triggering event, if you will, was short-selling. A series of reports were able to pick out some truly problem companies. In that regard there has been some impact in real financial terms and in the minds of investors, particularly in the US."

Following several SEC probes last year, five instances of investor fraud by US-listed Chinese companies have been probed by the regulator.

Bad apples

Zhongpin Inc, a pork processor from Changge, in Henan province, and six Chinese citizens were charged by the SEC in a civil lawsuit filed by the SEC on April 4 for insider trading in the company's Nasdaq-listed shares.

According to the US regulator, the six Chinese citizens, along with a British Virgin Islands trading entity operated by one of them, made profits of nearly $9.2 million in Zhongpin stock trades ahead of a March 27 announcement that Zhu Xianfu, its chairman, CEO and biggest shareholder, had offered to take the company private in a $520 million buyout.

Two days after the SEC's complaint was filed, assets of the six individuals and Prestige Trade Investments Ltd held in US brokerage accounts were frozen, preventing "millions of dollars from moving offshore", said Merri Jo Gillette, head of the SEC's Chicago office.

The SEC declined to comment about Zhongpin or any of its other cases, as they are ongoing investigations.

Following the SEC action, Zhongpin disclosed that a special committee of its board of directors would consider the privatization proposal, a review that is still ongoing, according to company disclosures.

Zhongpin has not used any of its filings so far to address the insider trading charges as it is not obliged to do so. The company, whose stock continues to trade on Nasdaq, did not respond to the requests for comments on the issue, when contacted.

Puda Coal Inc Chairman Zhao Ming and its former chief executive Zhu Liping were accused of cheating US investors by the SEC in a complaint filed on Feb 22. Zhao, the SEC claims, secretly transferred control of the company's main revenue source - the 90 percent indirect ownership of Shanxi Puda Coal Group Co in North China - to himself in September 2009, just weeks before that asset received a lucrative contract from the Shanxi provincial government to consolidate smaller mining companies. (Puda Coal is based in the province's capital, Taiyuan.)

Nearly a year later, in July 2010, Zhao sold 49 percent of Puda Coal to a private-equity fund controlled by State-owned investment firm Citic Group. The chairman also allegedly caused Shanxi Puda Coal to pledge the other 51 percent of itself as collateral for a $516 million loan, the SEC said. Zhao's dealings were allegedly carried out with the knowledge of Zhu, who was Puda Coal's CEO at the time.

According to the SEC's suit, filed in New York, the transfer deal turned Puda Coal into an "empty shell" before two public offerings of stock in the US during 2010. The company's board never approved the deal, nor was it disclosed to investors, whom Puda Coal misled by maintaining that it still owned 90 percent of Shanxi Puda, the SEC said.

The action against Puda Coal was the first since the SEC in 2011 began examining the process of reverse mergers, including how Chinese companies have used them to get listed as publicly traded entities on US stock exchanges. In a reverse merger, a private foreign company, usually small or midsize, merges with an existing US-based public shell company. The process is far less rigorous than going public through an IPO, and the SEC and other US regulators have questioned the accuracy of accounting practices at dozens of Chinese companies that have gained a US listing this way.

Puda Coal used a reverse merger to get its shares listed on the American Stock Exchange in late 2005. They were delisted from the Amex in September 2011 and now trade on the largely unregulated, privately run over-the-counter market in the US.

Coulson, whose CCG has advised Puda Coal in the past, said neither he nor his firm would comment on the SEC case against the Chinese company. Efforts to reach representatives of Puda Coal or the lawyers for Zhao and Zhu were also futile. The SEC is seeking the return of any ill-gotten gains the two officials may have made through the alleged scheme.

SinoTech Energy Ltd, a Beijing-based provider of oilfield services, along with CEO Xin Guoqiang and former chief financial officer Zhang Boxun, was accused by the SEC in an April 23 suit of misrepresenting the value of the company's assets and how $120 million in proceeds from its November 2010 IPO in the US was spent.

According to the SEC suit filed with a federal court in Louisiana, SinoTech told investors through regulatory filings that it had bought $94 million worth of lateral hydraulic drilling units - its main assets in conducting operations such as horizontal drilling and coalbed methane recovery - when in fact it had purchased only $17 million worth.

Chairman Liu Qingzeng was accused separately in the same SEC complaint of secretly withdrawing $40 million from SinoTech's bank account. The company didn't record the withdrawal and kept Liu as chairman even after he admitted the conduct, according to the SEC.

SinoTech didn't reply to requests for comment for this story, but in August 2011 the company reacted sternly to a claim posted on AlfredLittle.com that its "largest customers and suppliers are likely nothing more than empty shells with little or no sales or income."

"We are outraged by this blatantly self-interested, mercenary attempt to profiteer at the expense of SinoTech and its shareholders," Xin said on Aug 17, a day after the AlfredLittle.com posting, which caused SinoTech shares to plummet 41 percent and Nasdaq to suspend their trading. The CEO said the report was "riven with inaccuracies, fabrications and unsubstantiated allegations, and its conclusions are utterly without foundation. We stand by the integrity of our company."

While SinoTech sources say that the research report was a creation by short-sellers, the owner of the report AlfredLittle.com says it publishes "cutting-edge long and short investment ideas and research focusing on companies operating and doing business in China". It further adds that it is "primarily supported by the efforts of analysts and investors based in China".

Following the trading suspension in August, SinoTech shares were later suspended permanently and subsequently delisted from the Nasdaq on Sept 21. Two days later the company disclosed that Ernst & Young Hua Ming, the China affiliate of the top accounting firm, had resigned as its auditor, citing concerns over a SinoTech transaction with Liu. It also announced two more resignations - Zhang as chief financial officer and Liu Jing as chairwoman of the board's audit committee.

Zhang and Ernst & Young cited several reasons for their decisions, according to SinoTech. These included a belief that there may have been an unauthorized transfer in 2011 by Liu of a material portion of the company's cash from a Chinese bank account in the name of SinoTech's Chinese operating subsidiary to an account the chairman controlled.

China Natural Gas Inc and its Chairman Ji Qinan got into trouble with the SEC on May 14 for concealing the true purpose of the two short-term loans. The SEC said the company had secretly disbursed $14.3 million of its funds to Ji's son and nephew in January 2010. The deal was done at a time when Ji was the chief executive of China Natural Gas. Ji stepped down as CEO in October 2011 but still continues to be the company chairman.

Ji allegedly told directors of China Natural Gas, which is based in Xi'an, capital of Northwest China's Shaanxi province, that the loans involved a liquid natural gas project. According to the SEC's complaint, "this lie" was repeated to investors on May 10, 2010 during a conference call about the company's quarterly earnings.

China Natural Gas itself is accused of failing to properly report a $19.6 million acquisition of another gas company it made in the fourth quarter of 2008.

In its suit, the SEC has sought unspecified civil fines from China Natural Gas and a ban on Ji from serving as a public company officer or director. Trading of China Natural Gas shares, which had begun on Nasdaq in June 2009, was halted last September and the stock delisted in November.

Rebound in sight

After 18 months of anxieties - some well-founded, others overblown - over reverse mergers, short sellers, auditing fiascoes and alleged fraud, there are still some doubts over whether there will be a long-term pullback in IPO and other cross-border activities pertaining to equities. Some experts even say that the long chill could continue.

"There is a very deep bench of highly qualified Chinese companies that would like to list [in the US], but there is limited appetite among international investors until these issues are sorted out," said CCG's Coulson. He's quick to add, however, that his investor-relations firm knows of about 45 Chinese companies that are preparing a US listing, with half having begun the SEC application process.

Schechter, of Dragon Gate, believes that the Chinese companies' desire to trade on US exchanges, given the prestige and "cachet" it affords, is so strong that it can outweigh American investors' wariness. In time, many of the existing market players will want to get off the sidelines and back into China's dynamic market.

"A number of companies have approached us about preparing for an IPO" in the US within a year or two, Schechter says. The potential issuers are in "consumer products and services for the growing middle class", including healthcare and clean-technology products beyond solar energy, such as engines and fuel processing.

For numerous US-listed Chinese companies that have not run afoul of the rules, weakness in share prices is collateral damage from the scandals.

"It has definitely hurt," says Koo Shang-Hsiu, CFO of Nasdaq-listed Jiayuan.com International Ltd, China's leading online matchmaking service. "For US investors, it's often a matter of being unfamiliar with the Chinese market.

"But if you do due diligence properly, you'll find that there are some very good companies available at low valuations," he says. "Some investors have realized this and are enjoying the fruits of their investment."

josephboris@chinadailyusa.com

(China Daily 06/15/2012 page1)

Relief reaches isolated village

Relief reaches isolated village Rainfall poses new threats to quake-hit region

Rainfall poses new threats to quake-hit region Funerals begin for Boston bombing victims

Funerals begin for Boston bombing victims Quake takeaway from China's Air Force

Quake takeaway from China's Air Force Obama celebrates young inventors at science fair

Obama celebrates young inventors at science fair Earth Day marked around the world

Earth Day marked around the world Volunteer team helping students find sense of normalcy

Volunteer team helping students find sense of normalcy Ethnic groups quick to join rescue efforts

Ethnic groups quick to join rescue efforts

Most Viewed

Editor's Picks

|

|

|

|

|

|

Today's Top News

Chinese fleet drives out Japan's boats from Diaoyu

Health new priority for quake zone

Inspired by Guan, more Chinese pick up golf

Russia criticizes US reports on human rights

China, ROK criticize visits to shrine

Sino-US shared interests emphasized

China 'aims to share its dream with world'

Chinese president appoints 5 new ambassadors

US Weekly

|

|